Key Takeaways

- Crypto-backed mortgages allow you to leverage digital assets to buy property without selling them.

- They offer benefits like tax efficiency, faster approval, and portfolio diversification.

- However, crypto volatility and regulatory risks must be considered.

- Platforms like Nexo, Ledn, and Salt Lending provide custom solutions tailored to crypto investors.

What Is A Crypto-Backed Mortgage?

A crypto-backed mortgage is a type of home loan where digital assets serve as collateral instead of fiat cash or tangible assets. This allows crypto holders to borrow against their portfolios without liquidating their investments.

Source: Stratmor Group

How It Works

- Borrowers pledge their cryptocurrency to a lender.

- The lender locks the crypto in a secure custodial or escrow account.

- A fiat loan (e.g., USD) is issued to fund the real estate purchase.

- As long as borrowers meet repayment obligations, they retain ownership of their crypto assets.

If your collateral value drops due to market volatility, the lender may issue a margin call, requiring additional collateral to maintain the loan.

Blockchain’s Role In Mortgage Lending

Technology Powering Transparency

Blockchain plays a crucial role in making crypto-backed mortgages secure and efficient. Key benefits include:

- Smart contracts to automate loan execution and reduce paperwork.

- Immutable records for tamper-proof documentation.

- Decentralized systems that enhance transparency and reduce fraud.

As blockchain adoption increases across financial and property markets, crypto mortgages are becoming more mainstream.

A Glimpse Into the Past

In 2012, BTCJam emerged as one of the first platforms for Bitcoin-backed loans. By 2016, it had facilitated over 16,000 loans across 120+ countries, an early indication of the demand for crypto-collateralized lending.

The Crypto-Backed Mortgage Process

Step-by-Step Guide

1. Eligibility Requirements

Lenders usually accept popular cryptocurrencies like BTC or ETH. To mitigate risk, they may require over-collateralization—often 150% of the loan’s value.

2. Financial Vetting & Compliance

In addition to crypto holdings, lenders assess:

- Credit history

- Income stability

- Source of funds (for AML compliance)

Proper documentation is essential to verify that crypto assets are legally acquired.

3. Application and Collateral Transfer

- Choose a platform or lender offering crypto-backed mortgages.

- Transfer crypto assets to a designated custodial or escrow wallet.

This ensures that the lender can liquidate the collateral in case of default.

4. Property Appraisal and Loan Finalization

The lender appraises the real estate to determine its value. Once approved:

- Terms like interest rate and repayment schedule are finalized.

- Funds are disbursed in fiat currency.

5. Repayment and Collateral Monitoring

Repayment models vary:

- Interest-only loans with a balloon payment

- Traditional amortized loans

Lenders continuously monitor the crypto collateral. If its value drops below a threshold, a margin call is issued.

Why Choose Crypto-Collateralized Home Loans?

Preserve Your Crypto Investment

You don’t have to sell your digital assets, meaning you can still benefit from future price increases.

Potential Tax Benefits

Avoiding the sale of crypto helps defer or eliminate capital gains taxes, depending on your jurisdiction.

Faster, Flexible Approval

Traditional credit scores take a back seat. The value of your collateral matters more, helping borrowers with unconventional credit profiles get approved faster.

Risks & Considerations

Proceed with Caution

Crypto Market Volatility

Rapid fluctuations in crypto prices can lead to unexpected margin calls or asset liquidation.

Regulatory Uncertainty

Crypto regulations differ by region and are constantly evolving. Legal compliance is critical to avoid complications.

Complex Loan Terms

Be sure to understand:

- Repayment structure

- Margin call triggers

- Liquidation clauses

Read the fine print to avoid surprises.

Where to Get a Crypto-Backed Mortgage

Top Platforms For Real Estate Financing With Crypto

1. Nexo

- Offers loans in over 40 fiat currencies

- Flexible repayment options

- Instant approval process

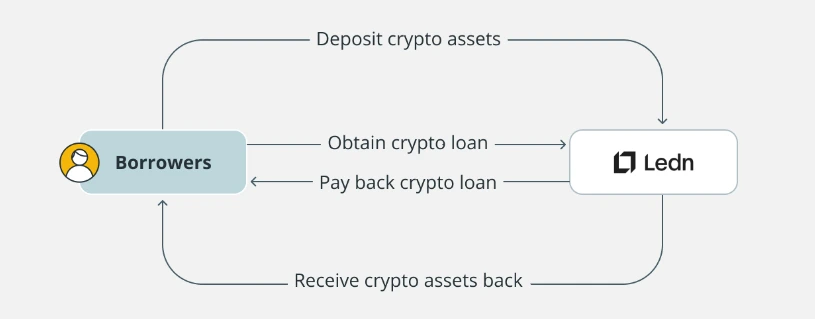

2. Ledn

- Specializes in Bitcoin-backed mortgages

- Allows clients to finance homes without selling their BTC

Source: Ledn

3. Salt Lending

- Facilitates real estate-backed loans with crypto collateral

- Offers a wide range of digital asset support

Key Criteria When Choosing a Platform

- Reputation: Look for trusted providers with solid track records.

- Security: Ensure funds are stored securely via multi-signature wallets or insured custodians.

- Interest Rates: Compare LTV (Loan-to-Value) ratios and APRs.

- Crypto Support: Make sure your preferred coin is accepted.

- Compliance: Confirm adherence to local financial regulations.

- Customer Support: Reliable service can ease the borrowing process.

FAQ

Can I use any cryptocurrency as collateral?

Most lenders only accept established cryptocurrencies like Bitcoin and Ethereum due to their liquidity and market stability.

What happens if my crypto loses value?

You may receive a margin call, requiring additional crypto to maintain the loan. If not met, your assets may be liquidated.

Will I owe taxes on a crypto-backed mortgage?

Possibly not. Since you’re not selling your crypto, you generally avoid triggering capital gains taxes. Consult a tax professional.

Can I still qualify with poor credit?

Yes. Many crypto mortgage platforms prioritize your collateral value over your credit score, making them accessible to more borrowers.