In a statement released on May 29th, the U.S. SEC’s Division of Corporation Finance said:

“Certain ‘Protocol Staking Activities’, such as staking on Proof-of-Stake (PoS) blockchains, do not need to be registered under the Securities Act of 1933, nor do they fall under its exemptions.”

The U.S. SEC Providing Clarity On Certain Protocol Staking Activities

Source: SEC

According to the SEC, staking rewards are seen as compensation for services, not profits from the “entrepreneurial or managerial efforts of others.” This language echoes the famous Howey Test, the SEC’s benchmark for determining what qualifies as a security.

The division also addressed custodial staking, clarifying that it is not considered a securities offering.

Custodians, they explained, act merely as agents, with no direct control over staking amounts or outcomes, and therefore are not engaging in activities that fall under securities regulations.

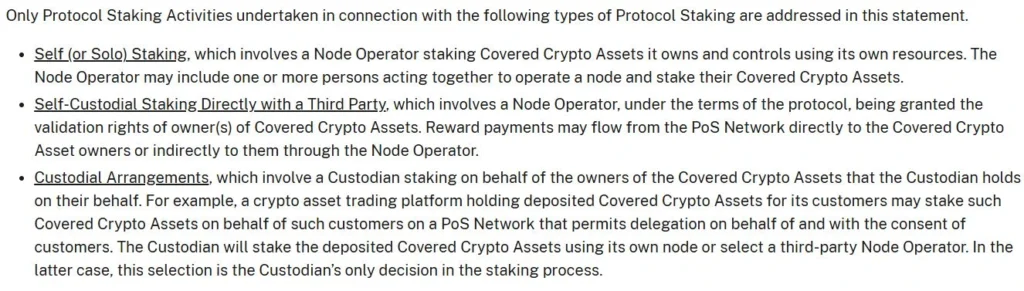

The guidance extended its non-security classification to certain ancillary services related to staking. These include:

These services, according to the SEC, are administrative or ministerial in nature, and thus do not contribute to the economic substance of an investment contract.

Importantly, this guidance does not address newer forms of crypto staking, such as:

The statement also emphasized that it “has no legal force or effect,” meaning it serves as internal guidance and not binding law.

Republican Commissioner Hester Peirce, who leads the SEC’s Crypto Task Force, praised the guidance. She emphasized that regulatory ambiguity had previously discouraged participation in staking among U.S. citizens.

Commissioner Peirce Talking About Staking

Source: www.sec.gov/newsroom

In Peirce’s view:

“Uncertainty about regulatory views on staking discouraged Americans from doing so for fear of violating the securities laws. This artificially constrained participation in network consensus and undermined decentralization, censorship resistance, and credible neutrality of proof-of-stake blockchains.”

In stark contrast, Democratic Commissioner Caroline Crenshaw criticized the guidance, calling it a misleading interpretation of the law. She argued that the statement fails to align with the Howey Test and relevant court precedents.

In her view:

“This is yet another example of the SEC’s ongoing ‘fake it till we make it’ approach to crypto. The staff’s analysis may reflect what some wish the law to be, but it does not square with court decisions on cryptocurrency staking.”

The guidance arrives after increasing pressure from various Web3 infrastructure providers and industry groups. During Solana’s Accelerate Conference in New York this May, participants called on the SEC to provide definitive rules for staking.

Though not legally binding, the guidance may influence future rulemaking, judicial decisions, and enforcement actions. For now, it offers a degree of regulatory relief for blockchain developers and validators operating in good faith.

Not officially. The SEC staff’s guidance suggests many types of staking are not considered securities, but this is not legally binding and could change with future court decisions or regulatory updates.

If you are involved in basic staking or staking-as-a-service, you’re likely on safer ground, but complex or emerging models like liquid staking may still face scrutiny.

The Howey Test determines whether a transaction qualifies as an investment contract, and therefore a security, based on whether there is an investment of money in a common enterprise with an expectation of profits from the efforts of others.