The GENIUS Act is under scrutiny from the U.S. banking lobby, particularly over concerns about interest-bearing stablecoins.

Section 4(a)(11) appears to ban interest payments but includes language that may allow legal workarounds.

Crypto leaders see interest-bearing stablecoins as the future of finance, while banks view them as a threat to the existing credit system.

Despite efforts from the Banking Policy Institute, most experts believe it’s too late to significantly amend the GENIUS Act.

The debate reflects a broader power shift from centralized finance to decentralized alternatives.

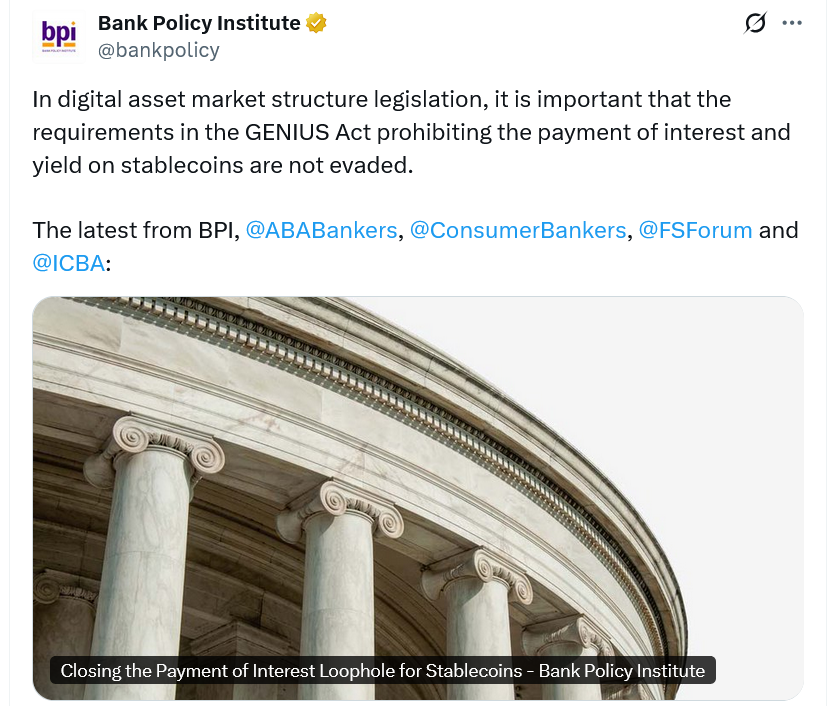

The Banking Policy Institute (BPI), a powerful voice in Washington backed by institutions like JPMorgan Chase, recently sent a letter to Congress arguing that the GENIUS Act contains loopholes that could allow stablecoin issuers to pay interest.

According to the BPI, this could destabilize traditional financial systems by redirecting deposits away from banks and increasing the cost of credit.

Source: X (@bankpolicy)

The BPI’s concern is rooted in a key provision of the GENIUS Act, Section 4(a)(11), which prohibits stablecoin issuers from offering any interest or yield solely based on the holding or use of the coin.

Yet legal experts argue the word “solely” introduces flexibility that could allow for third-party arrangements.

Aaron Brogan, founder of crypto-focused Brogan Law, notes that while the GENIUS Act appears strict on the surface, the language leaves room for interpretation.

Brogan explained:

“The word ‘solely’ is a powerful legal limiter. If there’s any additional basis for the interest beyond simple holding, it may not violate the law.”

This opens the door for crypto exchanges or platforms to structure interest-earning products around stablecoins, potentially bypassing the intended restrictions without technically violating the act.

Stablecoins offering competitive yields could lead users to pull their deposits from traditional banks. The BPI argues that such a shift could:

Increase lending costs

Reduce available credit

Destabilize bank-centric financial systems

Banks currently rely on customer deposits to issue loans and create credit. If those deposits flow into stablecoins instead, the traditional credit engine could slow down, potentially affecting Main Street businesses and household lending.

Various crypto leaders, including Coinbase CEO Brian Armstrong, have championed interest-bearing stablecoins as a financial innovation that empowers consumers. However, others urge caution.

Andrew Rossow, a policy attorney and public affairs expert, warns that the compliance burden around solvency, reserves, and anti-money laundering (AML) requirements is significant.

“Easy compliance is a myth,” Rossow said. “Stablecoin issuers would need to operate like banks, but without the oversight.”

Still, Rossow adds that an outright ban on interest may be more about protecting banks than ensuring consumer safety.

Despite banking efforts to influence lawmakers, many believe that changes to the GENIUS Act are unlikely.

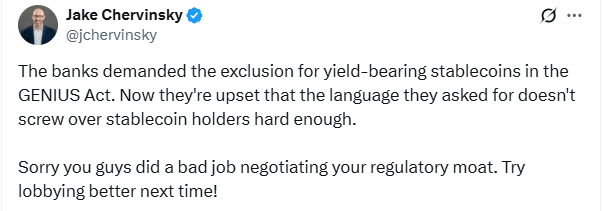

Jake Chervinsky, Chief Legal Officer at Variant, suggests that the current legislation already reflects compromises with the banking lobby.

Source: X (@jchervinsky)

Brogan draws a parallel between the current fight over stablecoins and past resistance to technological shifts, like the music industry’s backlash to MP3s.

“People used banks because they had no choice. Now, they have better options.”

In other words, the momentum behind DeFi may be too strong for traditional banks to counteract.

The GENIUS Act is U.S. legislation aimed at regulating stablecoin issuers, setting clear rules around reserves, compliance, and yield-bearing capabilities.

Banks fear that loopholes in the law could allow stablecoins to pay interest, potentially drawing deposits away from banks and threatening the traditional credit system.

Section 4(a)(11) prohibits paying interest solely for holding stablecoins, but legal experts argue the wording allows for workaround mechanisms through partnerships or added services.

It’s unlikely, according to legal experts and policymakers. The law already incorporates compromises with banking interests, and major amendments appear politically infeasible.